How to Setup a Chart of Accounts in Quickbooks Pro 2012

A chart of accounts is a complete listing of a company’s accounts and their balances. The chart of accounts is used to track how much money a company has, what a company owes and how much money is coming in or going out of the company. The chart of accounts categorizes your income, expenses, assets, liabilities and owner’s equity amounts into one list which is an essential part of a company’s financial reporting.

A basic chart of accounts is usually Easy Step Interview when you are creating your new Quickbooks Company File for the first time. During the set-up interview Quickbooks will ask you several questions to determine the type of company you are setting up.

Choose your Company’s industry and follow the onscreen instructions:

Once your basic chart of accounts is set-up you can add accounts at anytime, make accounts inactive that are no longer needed; or, delete accounts that have not been used.

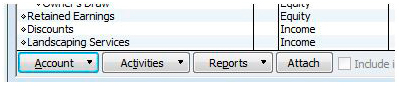

To add an account:

Go to the Lists menu and click Chart of Accounts.

Click on Account at the bottom of the list and click New.

In the next screen choose the Type of Account and click continue. Once you choose the type of account, a description of the account will display onscreen.

In the Account Name field, enter the name of the account; if you use account numbers enter the number in the Number field. Next, enter a short description of the account in the Description field.

If the account you are adding, is a Bank Account or Credit Card Account, you can enter the account numbers in this screen then, enter the opening balances.

To make this a subaccount, select the Subaccount of checkbox and then click on the drop down arrow to select the parent account. Often times a company will use subaccounts under a parent account to track different categories within the main account. For i.e.

• Marketing and Advertising

• Advertising Expenses

• Printing Costs

• Website Hosting

• Etc.

For income and expense accounts, you can choose a Tax Line from the drop down menu list or choose <not tax related>.

You can enter an opening balance if the Opening Balance button is displayed. Balance Sheet accounts generally require an opening balance to be entered when adding an account and are based on the balance as of your Quickbooks start date.

You can track reimbursed expenses as income by selecting the Track reimbursed expenses in: option, then click the Income Account from the drop down list and choose the appropriate income account to be used. Be sure the preferences are turned on for sales and customers in the preferences menu.

Click Next to save the account and to add another account or click OK to save the account and close the window.

To add more accounts, repeat the above steps.

Need QuickBooks training? Get 24 hours of QuickBooks Pro training tutorials.

Cindy McGuckin

Cindy McGuckin is an IT trainer with over 20 years of experience. Cindy currently manages the IT Training Department at Trident Technical College, she's a Member of the Association of IT Professionals, Charleston, SC chapter and the Treasurer of the South Carolina Association of Continuing Higher Education.Cindy is a Microsoft Office and QuickBooks expert and her online courses have received hundreds of 5-star reviews. Her no-nonsense approach to teaching complicated topics makes her classes engaging and interesting.